When most people think of life insurance, they automatically associate it with a worst-case scenario. We have been culturally conditioned to believe that life insurance is simply a monthly expense designed to cover funeral costs or to provide a financial safety net for dependents after death. In short: money you pay, but never actually get to enjoy during your lifetime.

In the United States, however, the mindset of middle and upper-class families is completely different. Within the American financial system, specific permanent life insurance structures are utilized as some of the largest and most efficient tools for wealth building, accumulation, and asset protection during your lifetime.

The open secret behind this strategy—heavily favored by business owners, professionals, and smart investors across the East Coast—is called IUL (Indexed Universal Life). In this article, we will demystify this tool and explain, without complicated financial jargon, how you can use the U.S. financial system to build tax-free wealth.

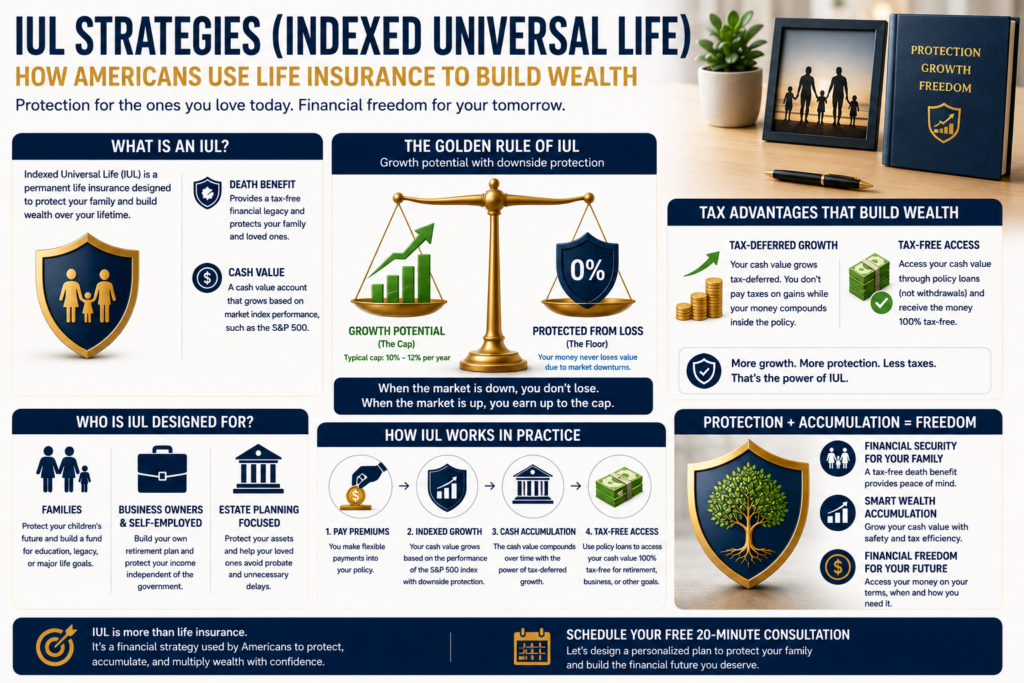

What is an IUL and how does it work in practice?

An Indexed Universal Life (IUL) policy is a type of permanent life insurance. This means that, unlike temporary term insurance (Term Life), it does not expire after 10 or 20 years; it stays with you for your entire life.

The primary advantage of an IUL lies in how your money is managed inside the policy. When you make your premium payments, the funds are split into two fundamental components:

The Death Benefit: The traditional coverage that guarantees immediate, liquid financial protection for your family and heirs if you pass away.

The Cash Value Account: A built-in accumulation and equity-building account. This is where the magic of wealth multiplication takes place.

The money allocated to your cash value account does not sit idle losing purchasing power to inflation. The accumulated dollars grow based on the performance of a major stock market index, such as the S&P 500 (the 500 largest companies in the U.S.). However, you are not buying stocks directly, which leads us to the most powerful safety feature of this product.

The Golden Rule of an IUL: Market Upside with Zero Downside Risk

Anyone who has ventured into the stock market knows that volatility can be intimidating. Watching your hard-earned savings disappear during a market correction or economic crash is a constant fear. An IUL solves this problem through a mechanism known as The Floor.

American insurance carriers guarantee that the growth of your cash value account has a permanent “floor” of 0%.

In practice: If the U.S. stock market plummets by 15% or 20% during an economic downturn, your IUL policy’s interest crediting simply stays at 0%. Your accumulated cash value does not drop a single penny. You are completely insulated from market losses.

The Balance (The Cap): In exchange for this absolute protection against negative years, the insurance company establishes a “cap” on gains (generally ranging between 10% and 12% per year). If the market surges by 20%, your account captures the return up to that maximum cap.

This positive asymmetry—capturing growth when the market rises and remaining safely locked in place when the market falls—creates a highly efficient compound interest effect over time.

The Tax Advantages: The Power of Tax-Free Growth

For anyone living and earning in the United States, taxation is a major hurdle to wealth accumulation. Standard investments, like traditional brokerage accounts or savings vehicles, face the bite of capital gains taxes. Because an IUL is legally classified as a life insurance policy, it enjoys unique tax advantages protected by the Internal Revenue Code that standard investments simply cannot match.

Tax-Deferred Growth

The earnings within your cash value account accumulate year after year without Uncle Sam taking a percentage in taxes. Because you do not pay annual capital gains taxes while the wealth builds inside the policy, your compounding growth accelerates significantly.

Tax-Free Distributions

This is the ultimate wealth strategy. When you decide to leverage your accumulated funds in the future—whether to supplement your retirement income, put a down payment on a property, or inject capital into your business—you can access your cash value through structured Policy Loans.

Because you are legally borrowing against your own cash value collateral rather than making a taxable income withdrawal, the IRS cannot tax the money. You receive the funds 100% tax-free.

Who is an Indexed Universal Life Policy For?

An IUL is not a one-size-fits-all product and is not ideal for every single financial situation. It is a strategic tool designed for specific profiles of individuals looking to advance their financial planning in the U.S.:

Family Providers: Who want to ensure their children’s futures are legally secure while simultaneously building a tax-free fund for college, inheritance, or legacy planning.

Self-Employed Professionals and Business Owners: Who lack corporate retirement matching (like a 401k) and want to build a private, reliable retirement nest egg separate from government-managed programs.

Individuals Focused on Estate Planning: Who understand the risks of leaving an unhedged estate exposed to judicial delays.

Keep in mind that, alongside accumulating wealth, an IUL fulfills the critical role of shielding your family with immediate liquidity. If you haven’t yet explored how the legal system handles physical assets and unmapped inheritance in Massachusetts, review our dedicated guide: [Asset Protection in Massachusetts: What happens to your bank accounts if you pass away? (Article 1)].

Designing a Customized Strategy

As we have seen, an Indexed Universal Life policy is a sophisticated financial structure that offers the best of both worlds: the unshakeable safety of permanent life insurance coupled with the tax-free growth potential of the U.S. markets.

However, an IUL policy cannot be purchased as an off-the-shelf retail product. It must be rigorously engineered and customized according to your current budget, age, health profile, and long-term financial goals. An improperly structured policy can undermine the efficiency of your returns.

As a licensed financial professional in the State of Massachusetts, my goal is to review your current financial landscape transparently and engineer a framework that aligns with your household budget and life milestones.

Protecting those you love requires a tailored strategy fit for your reality. Click here to schedule your free consultation and let’s structure the ideal plan for your family.

Published: June 2026