For almost everyone navigating the American financial system, the first major milestone is clear and often obsessive: building an excellent Credit Score. We download monitoring apps, track our points rising month after month, and celebrate when our score finally crosses the 750 or 800 threshold.

There is no denying that having excellent credit in the U.S. is phenomenal. It opens doors to financing vehicles at low interest rates, securing credit cards with generous limits, and eventually achieving the dream of buying a home. A high credit score brings a tangible sense of buying power, status, and stability.

However, this is precisely where the greatest hidden trap of personal finance lies: confusing your capacity to borrow money with actual financial security. A high score simply means you are an excellent manager of debt for the system—it does not guarantee that your household wealth will survive if an unexpected crisis occurs tomorrow.

True wealth and generational stability depend on much deeper foundations. In this article, we will look beyond the surface and reveal the 3 indispensable pillars required to build an unshakeable financial structure.

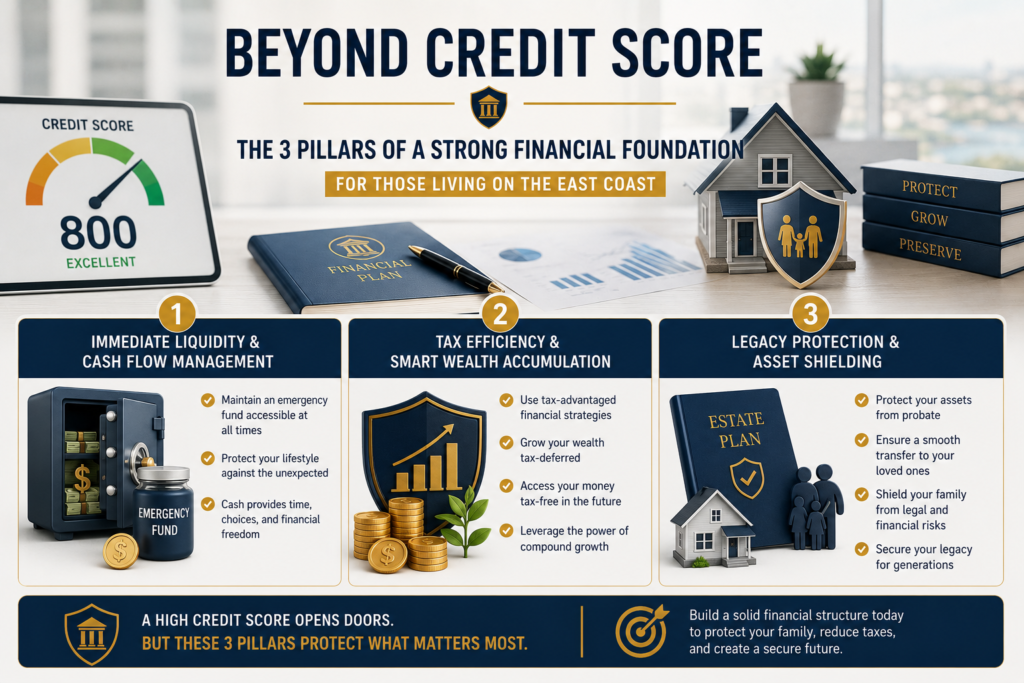

Pillar 1: Immediate Liquidity and Cash Flow Management

The modern lifestyle is heavily engineered toward credit-fueled consumption. It is incredibly easy to fall into the trap of financing an expensive lifestyle using credit cards and consumer loans, trusting that next month’s income will always arrive in time to cover the balances.

But what happens if your primary source of revenue stops abruptly due to a health issue, an injury, or an economic slowdown in your industry?

The first pillar of a rock-solid structure is Immediate Liquidity. Having an 800 credit score won’t pay your immediate bills if your cash is tied up or if you lack accessible liquid capital for emergencies. Strategic planning requires establishing a true emergency fund, engineered around your actual household cost of living, and kept in highly accessible accounts. Cash reserves buy you time, provide massive negotiating power, and prevent you from damaging your credit profile by relying on predatory financing during a crisis.

Pillar 2: Tax Efficiency and Smart Wealth Accumulation

Working hard and watching your bank account balances grow is highly rewarding. However, if you are accumulating your money in the wrong vehicles, the internal revenue system (IRS) will take a massive bite out of your wealth through capital gains taxes and ordinary income taxation.

Many high-earning professionals and business owners make the mistake of leaving excess capital strictly in standard checking accounts or traditional retail bank savings accounts, where the money underperforms inflation and remains heavily exposed to annual taxation.

The second pillar consists of leveraging advanced financial frameworks to your advantage, shifting a portion of your capital into structures that enjoy legally protected tax incentives. We are talking about vehicles that allow your wealth to grow on a tax-deferred basis (Tax-Deferred) and be accessed in the future completely free from income tax (Tax-Free). This is exactly how financially literate families multiply their wealth, utilizing the maximum compounding power of their dollars.

Pillar 3: Estate Shielding and Active Asset Protection

You can have the best credit score in the state, a beautiful primary residence, and robust bank accounts. Yet, if you do not have the third pillar activated, your family’s financial stability is built on fragile ground.

In the United States legal system, assets do not automatically or seamlessly transition to a spouse and children if the primary provider passes away. If you hold bank accounts, real estate titles, or vehicles registered solely under your individual name, those hard-earned achievements will be immediately frozen by state courts.

To release these assets to your rightful heirs, your family will be forced to file a costly lawsuit in the state estate court system. If you want to understand how this third pillar applies in practice to prevent your achievements from being held up by judicial bureaucracy, read our complete guide on How to protect your family’s future in Massachusetts and avoid the ghost of Probate.

The Mistake of Building a House from the Roof Down

Focusing exclusively on your Credit Score while ignoring the 3 pillars of financial architecture is the equivalent of obsessing over the paint and facade of a house while the concrete foundation beneath the soil is cracked. At the first sign of an economic storm or a personal emergency, the entire structure risks collapse.

Credit should be treated as an intelligent leverage tool to acquire assets, not as a crutch to sustain a lifestyle that lacks real structural safety nets behind it.

Securing Your Financial Foundation

The American financial system is one of the most prosperous and rewarding in the world, but it is entirely unforgiving to those who do not play by the rules of asset protection.

Aligning your cash flow, optimizing your tax liabilities legally, and activating the right estate shielding mechanisms is what guarantees that the fruit of your labor remains securely in the hands of your family—no matter what happens to the market or the broader economy tomorrow.

Setting up these 3 structural pillars requires a detailed, personalized analysis of your current financial landscape. Click here to schedule your free consultation for a 20-minute session, and let’s map out the blueprint to establish your definitive financial security.

Published: June 2026